The picture in the Japanese markets is beginning to resemble a slow but persistent phase shift in a system that has operated with artificial stability for decades. From being the savior of the monetary system during the Nixon shock with the largest monetary agreement in history, it is now expected to become the stinker of a leveraged financial system.

It seems that Japan will “explode” emphatically highlighting the end of the era of zero interest rates and cheap money.

The yen is hovering around 162 against the dollar, levels reminiscent of 1986, and the market is no longer just discussing further weakness, but whether the next major range is at 170 or even 200 yen/dollar.

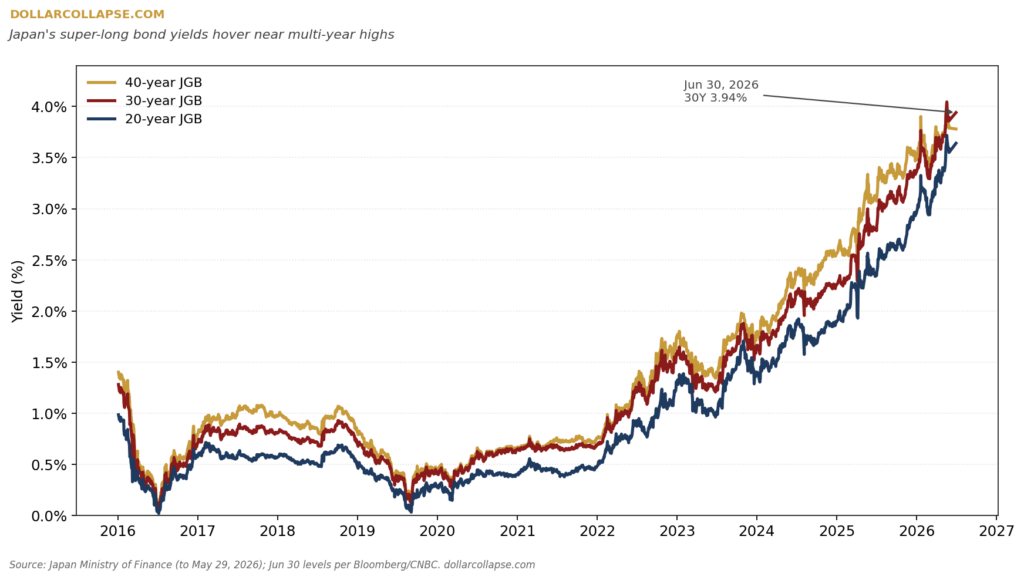

At the same time, the bond market is showing a parallel crack. Long-term Japanese government bond yields have been rising steadily, with the 30-year yield approaching 4%, in an economy where public debt is hovering between 240% and 260% of GDP.

For decades, this combination was considered almost impossible: a country with such high debt and such low financing costs. But now that balance is starting to shift.

The story behind this transition actually begins in 1985 and the Plaza Accords of 1985, when the sharp appreciation of the yen put pressure on Japan’s export-oriented model.

The Bank of Japan’s response was an aggressive easing that, rather than stabilizing the economy, contributed to the creation of the great bubble of the late 1980s.

When that collapsed in the early 1990s, Japan never returned to a “normal” monetary policy regime. Successive waves of intervention followed.

Zero interest rates in the late 1990s, the first QE in 2001, and then the big turn in 2013 with Haruhiko Kuroda and the QQE (Quantitative & Qualitative Easing) policy, where the central bank began massive purchases of government bonds and ETFs, gradually transforming itself into the dominant player in the very market it is supposed to regulate.

The result of this long journey is that today the Bank of Japan does not function simply as a central bank, but as the main financier of the Japanese state.

Its balance sheet has reached levels comparable to the country’s GDP, while its presence in the bond and equity markets remains decisive.

The tipping point of the balance

But this balance is beginning to be tested from two directions at once. On the one hand, the currency is weakening in a persistent and almost unequivocal way.

Despite interventions of the order of 11.7 trillion yen, or about 72.8 billion dollars, the yen continues to decline. On the other hand, the yield curve itself is starting to reprice risk, as the BOJ is forced to move from absolute suppression of interest rates to a very gradual normalization of monetary policy.

The increase in the base rate to 1%, the highest level in the last 31 years, has not managed to fully stabilize the picture.

At the same time, the central bank continues to buy about 2 trillion yen yen bonds per month, maintaining a hybrid monetary intervention regime where tightening and support coexist.

The contradiction is fundamental:

- if interest rates rise more aggressively, the cost of servicing a debt of more than 240% of GDP becomes explosive.

- If interest rates do not rise, the currency continues to depreciate, fueling inflation and eroding confidence.

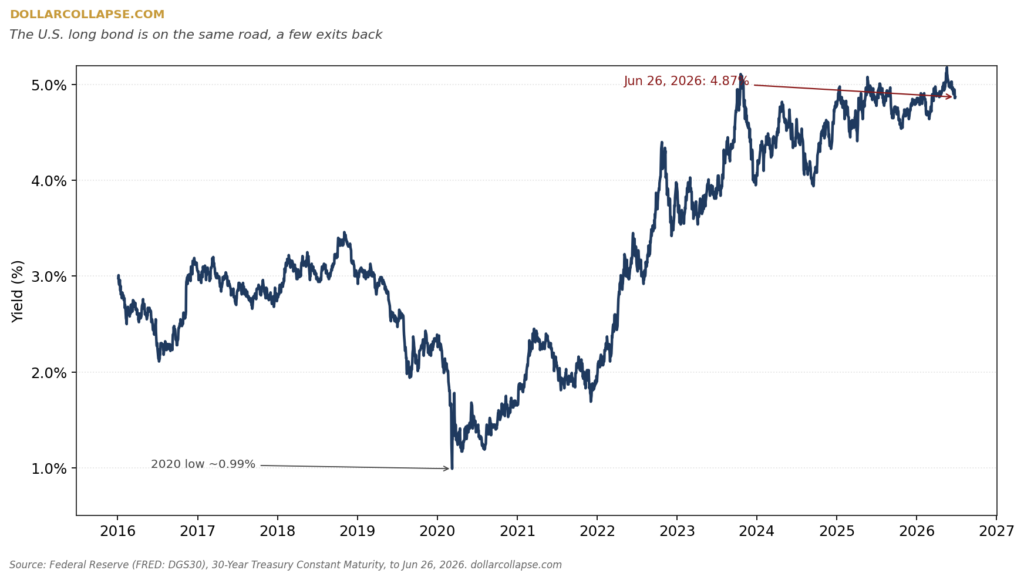

The risk of contagion for the US economy

But Japan’s story is not confined to its borders. The real point of interest lies in its connection to the United States.

The US is facing a public debt of nearly $40 trillion, while annual interest payments have already exceeded $1 trillion.

The financing of this system relies on one crucial factor: continued demand for US government bonds from abroad.

Japan remains one of the largest holders of Treasuries, with over $1 trillion. This means that any pressure on the yen is not just a local monetary phenomenon, but potentially a factor in the reallocation of capital in the global system.

If Tokyo needs to support its currency for an extended period, the need for dollar liquidity could lead to changes in the composition of its reserves.

It doesn’t take a massive liquidation to shift the balance. In markets of this size, even small changes in net flows can affect how risk is priced, especially in an environment where US debt issuance remains high and persistent.

The end of risk-free assets

The most crucial element, however, is that this interaction between Japan and the US is not direct, but mediated by expectations.

For decades, the fundamental assumption of the markets has been that the government bonds of the major economies are risk-free assets.

What is beginning to be tested is not solvency, but the pricing of this so-called risk-free status.

If this perception begins to change even marginally, the result will not necessarily be a default or otherwise technical bankruptcy, but a repricing of the cost of capital on a global scale.

And in this scenario, Japan is not the end point of the horror story. It is the point from which the crisis is expected to become universal and affect the entire planet…