A mysterious $580 million bet, completed just 15 minutes before Trump’s critical tweet on Iran, is sparking shocking suspicions of a “spoken” manipulation ring.

The 27 seconds that preceded the state intervention irreparably expose the credibility of international markets, revealing how some “invisible” traders made a fortune with surgical timing.

This is a rigged robbery that points directly to the White House background, turning oil into the field for the largest insider trading of the decade.

Oil traders took bets worth half a billion dollars about 15 minutes before Donald Trump’s tweet, in which he spoke of “productive” talks with Iran, sending crude prices tumbling, causing volatility in other assets as well.

In particular, about 6,200 futures contracts for Brent and West Texas Intermediate changed hands between 6:49 a.m. and 6:50 a.m. New York time on Monday, just a quarter of an hour before the US president’s tweet on Truth Social that there had been “productive talks” with Tehran in recent days to end the war in Iran.

The notional value of these trades was $580 million, according to Bloomberg data. Trading volumes for Brent and WTI rose sharply at the same time, 27 seconds before 6:50 a.m.

Futures tracking the S&P 500 index rose, with volumes increasing significantly during that time frame. It was not clear whether one or more entities were behind Monday’s trading.

Trump’s announcement at 7:04 a.m. triggered a sharp sell-off in global energy markets and a rise in S&P 500 futures and European stocks as investors trimmed bets on a prolonged conflict.

The well-timed trades were reminiscent of the wave of large and highly profitable bets on the Polymarket prediction market on the timing of U.S. strikes in Iran and Venezuela in recent months.

White House spokesman Kush Desai said: “The sole priority of President Trump and his administration is to do what is best for the American people.” He added: “The White House does not tolerate any government official engaging in insider trading, and any suggestion that officials engage in such activity without evidence is baseless and irresponsible journalism.”

Several hedge funds noted that this was one of several examples in recent months of large trades taking place before official government announcements.

In a post on X later Monday, Iranian parliament speaker Mohammad-Bagher Ghalibaf denied that negotiations were taking place between Washington and Tehran, sending global stocks tumbling and energy markets surging again.

He added, “Fake news is being used to manipulate the financial and oil markets and to escape the quagmire in which the US and Israel are trapped.”

There was a sharp move in the TTF, the European natural gas benchmark, around the same time. Brent futures and options markets had seen significant inflows” from funds in recent weeks. Given the price reaction, it seems that almost everyone was long. That’s almost a prerequisite for such a violent move.

Do the markets trust the president?

In this environment, one must ask: Do the markets trust the president? On Saturday, March 21, President Donald Trump said he would bomb Iranian political infrastructure if it did not open the Strait of Hormuz.

Yesterday morning, he said the bombing would not proceed because of (no capitalization) “in-depth, detailed and constructive” talks with Iran to end hostilities. Despite Iranian state media denying that there had been any talks, U.S. stock markets surged, bond yields fell slightly, Brent prices fell 10%, and the Vix volatility index fell sharply.

But why? The question must be asked, because we have seen this play out before.

Just two weeks ago, the president declared that the war with Iran was “almost over,” claiming that Iran “has no navy, no communications, no air force. Their missiles are scattered.” Risk assets rose sharply, and oil fell then too.

And every word that came out of the president’s mouth turned out to be nonsense. A day later, stocks continued to fall, oil continued to rise, and bond yields continued to rise. And of course, the president has a strong incentive to say that peace is coming.

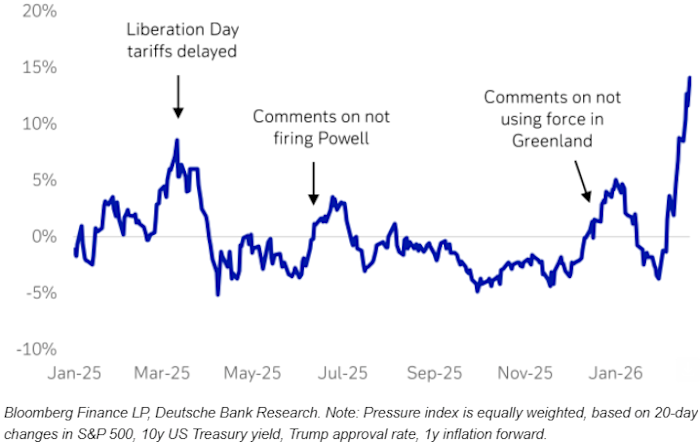

Maximilian Uleer and his team at Deutsche Bank have developed a simple and useful index of pressure on the president, a weighted measure that consists of four-week changes in the S&P 500 index, the 10-year U.S. Treasury yield, short-term inflation expectations, and the president’s popularity. The pressure is intense.

Three explanations

So why is the market responding to the “boy who cried peace”? Three explanations:

1. The president’s comments, while we can be fairly certain they are based on nothing at all, are an important signal of intent. The president seems to be genuinely seeking a way out, rather than seeking escalation out of frustration. This is risk-averse.

2. If investors are, for example, 80% certain that the president is just making things up, the remaining 20% probability is enough to move asset prices. No one wants to be on the wrong side of the price of oil on the day the strait opens wide.

3. Traders (human and machine) need reasons to trade. Presidential comments do the job, even if they are almost certainly “noise.” You buy on the news, then sell, take a profit, and call it a day.

We can fully explain yesterday’s market move without assuming that anyone considers the president a reliable source on the war.

A very useful “natural experiment” in gold

One of the most difficult questions in global markets in recent years is what exactly has driven gold’s impressive rise.

The price of gold had a good year in 2024 and a great one in 2025, before skyrocketing in early 2026. Because gold is not an industrial metal and has, let’s say, an erratic relationship with both inflation and the business cycle, there is room to attribute its rise to anything: dedollarization, fiscal devaluation, geopolitical disintegration, or even… sunspots.

The general view is that gold went through several phases: central banks around the world bought more after Russia froze its dollar reserves; then institutional investors added a little more to their portfolios as a hedge, as the traditional diversification properties of bonds were being weakened by inflation and central bank yield suppression; and then retail investors saw the price rise and got in on the action.

It was a great investment. But how much of this retail excitement and the general speculative frenzy has contributed to the price of gold? Good question.

Since the war began, gold has not risen as “safe havens” are supposed to do, but has fallen, like other riskier assets, and more so.

The extent of this decline, about 15% since the start of the war, came as a surprise to many, including us.

Yesterday’s (23/3) rally reinforced this momentum: the day began on a fearful note over Trump’s threats to bomb Iranian energy infrastructure.

Gold prices fell along with stocks. When Trump said the bombings were being called off due to successful peace talks, gold rallied. When Iran denied that talks had taken place, gold fell a bit. For now, gold is simply a high-risk asset.

One could argue that higher real interest rates and a stronger dollar explain gold’s weakness.

An additional factor with potential downside implications for gold is the possibility of increased selling by central banks.

In early March 2026, the governor of Poland’s central bank proposed a plan to sell or revalue part of its gold reserves to finance defense spending, aiming to raise $13 billion.

The impact of high oil prices, pressure on non-oil-producing countries’ foreign exchange reserves, rising defense spending, and geopolitical risks, combined with still-high gold prices, could encourage further official sector selling.

Incidentally, Poland’s central bank publishes reports like this one. If even they think it might be time to sell gold, this seems like a pretty significant signal.